Structured Settlement vs. Selling Other Assets: Which Should You Tap First When You Need Cash?

When you need a lump sum, a structured settlement isn't your only option. We compared the true effective costof six ways to access cash — from home equity loans to 401(k) withdrawals — using real 2026 rates. The answer isn't what most people expect.

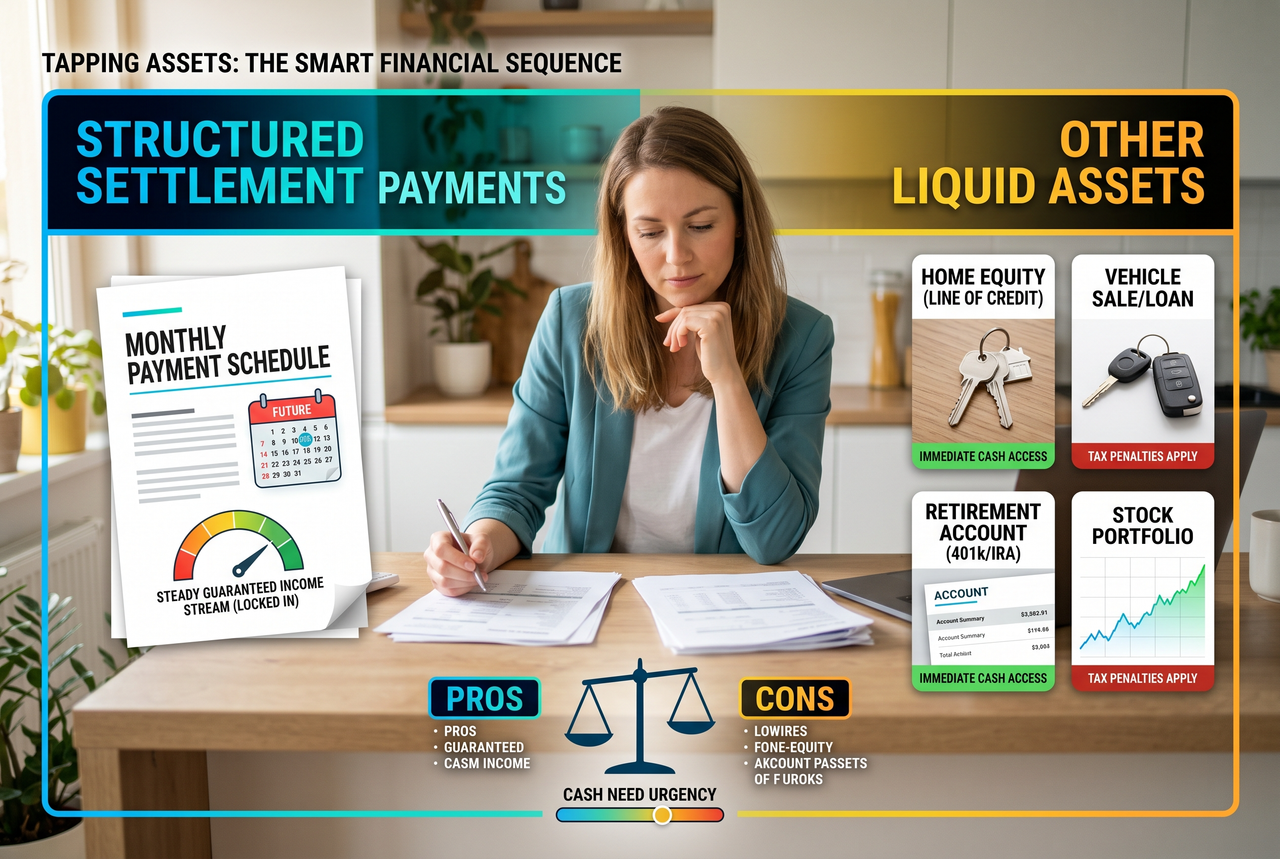

Quick Answer: The Decision Hierarchy

Based on effective cost analysis using June 2026 rates, here's the optimal order to tap assets when you need cash:

- 1.Home Equity Loan/HELOC — 8.13% APR, keep your settlement intact

- 2.Personal Loan — 12.28% average APR, unsecured, fast

- 3.Partial Settlement Sale — 14.7% effective discount rate (sell only what you need)

- 4.Credit Cards — 24.48% cash advance APR (emergency only)

- 5.401(k) Withdrawal — 35-45% effective loss (absolute last resort)

- 6.Life Insurance Sale — 50-75% of value lost (only if policy unneeded)

However, if you don't qualify for loans (no home equity, poor credit), selling a structured settlement may be your best — or only — option. That's OK. The key is getting a fair rate.

The True Cost Comparison: 6 Ways to Access Cash in 2026

Most people focus only on the interest rate or discount rate. But the true cost includes taxes, penalties, lost future value, and risk to other assets. Here's the complete picture:

Structured Settlement Sale

Time to funds: 45-90 days

14.7%

effective cost

Home Equity Loan (HELOC)

Time to funds: 2-6 weeks

8.13%

effective cost

Personal Loan

Time to funds: 1-7 days

12.28%

effective cost

401(k) Early Withdrawal

Time to funds: 3-10 business days

35-45%

effective cost

Credit Card Cash Advance

Time to funds: Immediate

24.48%

effective cost

Life Insurance Policy Sale

Time to funds: 2-4 weeks

50-75% loss

effective cost

Deep Dive: Understanding Each Option

🏠 Option 1: Home Equity Loan / HELOC

If you own a home with equity, this is almost always your cheapest option. The national average home equity loan rate in June 2026 is 8.13%(Bankrate data). You keep your structured settlement payments flowing, borrow against your home's value, and repay over 5-30 years.

The catch? Your home becomes collateral. If you can't make payments, you face foreclosure. And you need sufficient equity (typically 15-20% after the loan), decent credit (680+), and verifiable income. Many structured settlement holders don't qualify because their settlement income may not count as “verifiable income” for traditional lenders.

The Math on $50,000:

HELOC at 8.13% over 10 years = $60,927 total repaid ($10,927 in interest). Your settlement continues paying you the entire time.

💳 Option 2: Personal Loan

The average personal loan rate in June 2026 is 12.28% for borrowers with good credit (Yahoo Finance/Bankrate). With excellent credit (720+), you could get rates as low as 6.74% (Wells Fargo). With poor credit (below 640), expect 25%+ or denial.

Personal loans are unsecured — no collateral needed. Funding can happen in 1-7 days. The downside: loan amounts typically cap at $50,000-$100,000, you need provable income, and the monthly payments start immediately. If your structured settlement is your primary income, some lenders will count it — but many won't.

The Math on $50,000:

Personal loan at 12.28% over 5 years = $67,058 total repaid ($17,058 in interest). No asset lost, but monthly payment of $1,118.

⚖️ Option 3: Structured Settlement Sale

Based on our Transparency Index analysis of 2,417 transactions, the national average discount rate is 14.7%. The best buyers charge 9-11%, while predatory buyers charge 20%+.

The unique advantage: no credit check, no income verification, no monthly payments, no collateral risk. You receive a tax-free lump sum (for personal injury settlements under IRC 104). The court must approve the transfer, providing a layer of consumer protection no other option offers.

The disadvantage: you permanently give up future payments. If you sell $100,000 in future payments at a 14.7% discount rate, you might receive $62,000-$68,000 today (depending on payment timeline). Those payments are gone forever.

Critical insight: You can do a partial sale. Sell only the payments you need to access, and keep the rest flowing. Our 60/40 Rule™ says: if you're offered less than 60% of face value, the rate is above industry average. Use our Settlement Decision Score™ tool to grade any offer.

The Math on $50,000 (face value of payments sold):

At 14.7% avg discount rate: receive ~$33,500 today for $50K in future payments over 5 years. At best rate (10%): receive ~$38,800. At worst (20%): receive ~$28,200. Tax-free for PI settlements.

🏦 Option 4: 401(k) Early Withdrawal

This is where most people get devastated without realizing it. If you're under 59½, you pay a 10% early withdrawal penalty plus federal income tax (22-37% depending on bracket) plus state income tax (0-13%). The total effective cost is typically 35-45% of what you withdraw.

Withdraw $50,000 from your 401(k) at age 40? You'll owe approximately $5,000 in penalties + $11,000-$18,500 in federal tax + $0-$6,500 in state tax. That's $16,000-$30,000 gone to the IRS — and you've also lost decades of compound growth on that money.

The hidden cost: $50,000 withdrawn at age 40 would have grown to approximately $217,000 by age 65 (assuming 6% annual returns). You're not just losing $50K — you're losing $217K in retirement security.

The Math on $50,000:

Take home: ~$28,000-$35,000 after penalties + taxes. Lost future value: ~$217,000 by retirement. Effective cost: 35-45% immediate + lost compounding. This is almost always worse than selling a structured settlement.

💸 Option 5: Credit Card Cash Advance

The average cash advance APR in 2026 is 24.48% (WalletHub), and interest starts accruing immediately — no grace period. Plus a 3-5% upfront fee. This makes it one of the most expensive forms of borrowing that exists.

The only advantage: instant access, no approval process beyond your existing credit limit. This makes sense only for tiny amounts ($500-$2,000) in genuine emergencies when you can repay within 30 days. For anything larger or longer, you'll enter a debt spiral.

The Math on $10,000:

$10K cash advance at 24.48% + 4% fee = $10,400 day one. If paid over 2 years: $12,928 total. If minimum payments only: could take 10+ years and cost $15,000+ in interest.

📋 Option 6: Life Insurance Policy Sale (Life Settlement)

If you have a life insurance policy with cash value, you can sell it on the secondary market. Typical payouts are 25-50% of the death benefit— meaning you lose 50-75% of the policy's face value. The buyer takes over premium payments and collects the death benefit when you pass.

This only makes sense if: you no longer need the coverage (no dependents), you can't afford premiums, or the policy is about to lapse anyway. For most people with structured settlements, this is a worse option than a partial settlement sale.

The Math on $200,000 death benefit policy:

Typical life settlement payout: $50,000-$100,000 (25-50% of face). You lose insurance coverage entirely. Partial tax liability on gains above your cost basis.

The Decision Framework: When to Sell Your Settlement

Based on our analysis, selling a structured settlement makes financial sense when:

✅ Sell your settlement when:

- You don't own a home (no HELOC option available)

- Your credit score is below 640 (personal loans will be 25%+ or denied)

- You need more than $50K (beyond typical personal loan limits)

- You can't verify income for traditional lenders

- You need funds for a specific investment that will return more than the discount rate

- The discount rate offered is under 12% (better than most personal loans)

- You can do a partial sale and keep some payments flowing

❌ Don't sell your settlement when:

- You have home equity and qualify for a HELOC at 8%

- The amount you need is small ($5K-$20K) and a personal loan covers it

- You're being pressured by a buyer (use our 3-Day Cooling Test™)

- The discount rate offered exceeds 18% (predatory territory)

- Your need is temporary and you'll regret losing payments in 6 months

- You haven't gotten at least 2-3 competing quotes

The key insight most articles miss: these options aren't always mutually exclusive. You might take a small personal loan for an immediate need AND do a partial settlement sale for a larger expense. Or use a HELOC for part and sell a portion of payments for the rest. The goal is minimizing your total cost of capital.

Real Scenario: You Need $40,000 for Medical Bills

Let's say you have a structured settlement paying $2,500/month for the next 10 years ($300,000 total remaining) and you need $40,000 now for medical bills. Here's what each option actually costs you:

| Option | You Get | Total Cost | What You Lose |

|---|---|---|---|

| HELOC (8.13%) | $40,000 | $8,741 interest (10yr) | Nothing — settlement continues |

| Personal Loan (12.28%) | $40,000 | $13,646 interest (5yr) | Nothing — settlement continues |

| Partial Settlement (14.7%) | $40,000 | ~$18,000 in discount | ~$58K in future payments (2 years' worth) |

| 401(k) Withdrawal | $40,000 | ~$22,000 tax + penalty | $173K in future retirement growth |

| Credit Card Advance | $40,000 | ~$22,500 interest (3yr) | Monthly payment burden + credit score damage |

Bottom Line for This Scenario:

If you qualify for a HELOC, take it — you save $9,000+ vs. a settlement sale and keep all your payments. If you don't qualify for loans, a partial settlement sale at a fair rate (under 13%) is reasonable and better than raiding retirement or using credit cards. The worst option by far is the 401(k) withdrawal — you lose money on three levels (penalty, tax, and lost compound growth).

Applying The 60/40 Rule™ to Your Decision

If you do decide to sell, use our 60/40 Rule™: any offer below 60% of your remaining payments' face value means you're being charged above the industry average discount rate. For the scenario above ($58K in payments sold), you should receive at least $34,800 (60%). Getting $40,000 (69%) would indicate a fair-to-good rate.

Always get at least 2-3 quotes. Our Transparency Index data from 2,417 transactions shows that getting even one competing quote saves the average seller $8,200.

Not Sure Which Option Is Right for You?

Tell us about your situation and we'll help you understand your options — including whether selling makes sense or if there's a better alternative. Free, no obligation, completely independent.

Frequently Asked Questions

Is selling a structured settlement tax-free?

For personal physical injury settlements, yes — the lump sum remains tax-free under IRC Section 104(a)(2). This is a major advantage over 401(k) withdrawals or life insurance sales which trigger tax events. Workers' compensation settlements are also tax-free. However, punitive damage portions or non-physical injury settlements may have tax implications.

Can I sell just part of my structured settlement?

Yes — and you should strongly consider this over a full sale. You can sell a specific number of payments (e.g., 24 months of payments) while keeping the rest intact. This is analogous to taking a smaller loan rather than emptying your entire savings account. Most buyers offer partial sales, though some pressure you toward full sales because it's more profitable for them.

Why not just take a 401(k) loan instead of a withdrawal?

A 401(k) loan (not withdrawal) is actually a reasonable option if your plan allows it. You borrow from yourself, pay yourself interest, and avoid penalties. The limit is typically 50% of your balance or $50,000 (whichever is less). The risk: if you leave your job, the loan may become due in full within 60 days or convert to a taxable withdrawal.

What discount rate should I accept?

Based on our Transparency Index data: rates under 10% are excellent (grade A), 10-13% is fair (grade B), 13-16% is average (grade C), and anything above 16% is above average to predatory. Use our Settlement Decision Score™ to grade your specific offer.

How long does it take to sell a structured settlement?

Typically 45-90 days from signing paperwork to receiving funds. The biggest variable is court scheduling — a judge must approve the transfer under your state's Structured Settlement Protection Act. This is actually a consumer protection feature: it ensures the sale is in your best interest. States like New York (67 days average) take longer than Ohio (31 days) or Florida (35 days).

The Bottom Line

There's no universally “right” answer — only the right answer for your situation. A structured settlement sale at 11% is objectively cheaper than a credit card advance at 24% or a 401(k) withdrawal at 40%. But a HELOC at 8% beats all of them if you qualify.

The structured settlement industry wants you to think selling is your only option. Traditional financial advisors want you to think selling is always wrong. The truth is in the middle: it depends on your alternatives, the rate you're offered, and what the money is for.

Whatever you decide, never accept the first offer. Our data shows a single competing quote saves the average seller $8,200. And apply our 3-Day Cooling Test™: if after 3 days you still feel the same urgency, the decision is rational. If the urgency was manufactured by a buyer, you'll feel different by day 3.

Sources: Bankrate (home equity rates, June 2026), Yahoo Finance/Bankrate (personal loan rates), WalletHub (credit card cash advance APR), IRS.gov (401k penalty rules), NASP (structured settlement discount ranges), SettlementDecisions.com Transparency Index (2,417 court-approved transactions).

Published: July 1, 2026 | Author: SettlementDecisions.com Research Team

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Consult a qualified financial advisor before making decisions about your structured settlement or other assets.